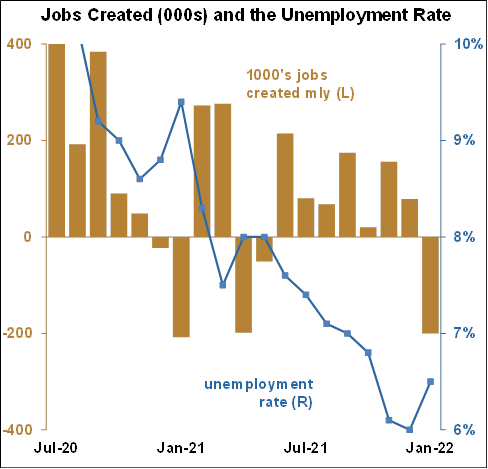

Let’s take a closer look at the January employment report.

As previously noted, the economy added an incredible 467,000 jobs in January, far above estimates of 150,000. Recently, the White House along with several analysts, suggested the number could have even been negative because of Omicron. In addition, the February 2nd ADP report showed a shocking drop of 301,000 jobs. Something feels amiss here.

Moreover, the revisions to the prior two months strain the limits of credibility.

- November job gains were revised up 398,000 from 249,000 to 647,000

- December job gains were revised up 311,000 from 199,000 to 510,000.

- Total revisions for the two months rose 709,000, a truly remarkable amount. The average revision for the two months was 355,000.

- Steve Liesman, senior economics reporter for CNBC said this morning regarding the revisions, “I’ve never seen anything like this."

How remarkable are those revisions? Well in the 11 years from the Great Recession to Covid, the average monthly job gain was 183,000. The revisions for November and December averaged 355,000. These were the number of people the Bureau of Labor Statistics (BLS) missed on the first count. Therefore, the average revisions for November and December of 355,000 were nearly twice as large as the average gain over the previous 11 years. What gives?

Part of the outsized revisions may have been caused by the BLS “benchmark” and seasonal adjustment updates (the reading of the technical details is a sure cure for insomnia). According to the BLS release, “some large revisions to seasonally adjusted data occurred with the updated models; however, these monthly changes mostly offset each other.” The keyword there is “some”. Apparently, it is unknown exactly how much the 709,000 revisions were due to the seasonal adjustment update, thus the skepticism.