Another analogy to illustrate the situation would be to think of the economy as a tide going out… it is “receding.” When it stops receding, the recession is over, but it’s nowhere near back to high tide.

A final analogy would be a sick patient whose fever gets worse and worse every day – their health is in recession. When the fever stops climbing, the patient’s health is no longer receding, but the patient is still very sick with a very high fever.

The end of the recession also coincides with the start of the recovery, and the economy will be growing again, probably very fast at the beginning. But it raises the question as to “how long will it take for things to get better? How long will it take to get back to where we were?”

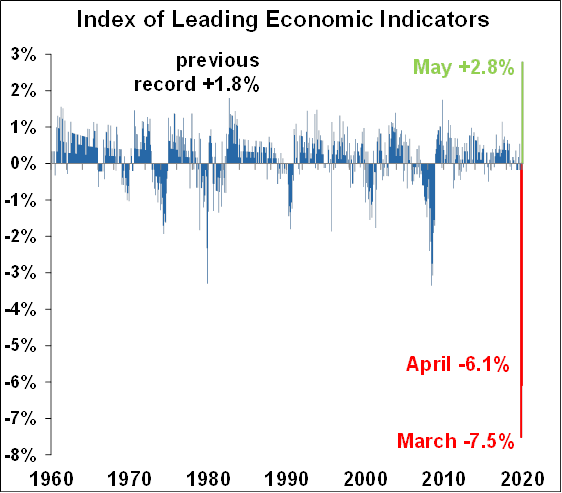

The answer is, unfortunately, probably a long time. Our broadest measure of the health of the economy is Gross Domestic Product (GDP), which is the value of all that is produced by the economy. The chart below shows the recent history of GDP in recessionary periods. Each line represents a recession labeled with the corresponding year. Each recession starts at quarter 0, then each recession ends when its curve hits bottom, and then each curve starts turning back up into the recovery. When the curve gets back to where it started, the economy has reached the GDP level just before the recession started, and it has fully recovered. The table corresponds with the different recessions but also adds five more recessions going back to WW-II. On average, it takes 6.3 quarters to recover, and if we strip out the extraordinarily long ’08 recession, the average is 5.5 quarters. Given these historical patterns, it’s likely that the recovery will take at least seven or eight quarters which would put us well into 2022 until we have returned to what it was like before COVID.