In the complex world of business, outstanding balances can be a major headache, casting a shadow on a company's financial health and operational efficiency. While they may seem like simple numbers on a financial statement, their impact is far-reaching. This article will explore the multifaceted impacts of outstanding balances, both direct and indirect. From accounting implications to the ripple effects on daily operations and growth aspirations, understanding these nuances is essential for any business that wants to thrive in today's competitive environment.

Understanding the Impact of Outstanding Balances on Business

December 27, 2023

Direct and Indirect Effects of Outstanding Balances on Business Health

An outstanding balance, while often perceived as a mere accounting term, can be a pivotal driver in the holistic health and growth trajectory of a business. The influence it wields stretches beyond financials, shaping a business's operational strategies, relationships, and future planning. In this deep dive, we dissect the multifaceted impact of outstanding balances, underscoring their significance through real-world examples and data.

Direct Impacts

Liquidity and Working Capital Constraints

Liquidity, often considered the lifeblood of any business, can be significantly affected by mounting outstanding balances. Every unpaid invoice directly reduces the available working capital, making daily operations challenging. This constraint means funds that could have been reinvested into the business remain locked away.

Case Study: A local manufacturer faced $200,000 in outstanding balances from various clients, preventing them from purchasing essential raw materials and stalling production for weeks.

Financial Strains from External Borrowing

Outstanding balances often force businesses to turn to external sources of financing, leading to increased borrowing costs. These additional costs, such as interest payments and other finance-related fees, eat into a company's profits. According to a study by QuickBooks, 31% of small businesses resort to such external financing due to unpaid invoices, typically at average interest rates ranging from 4-6%. Tightened cash flows further push businesses towards unplanned borrowing, which might come with even steeper interest rates. Such unplanned debt not only incurs more costs but can also divert funds from essential business operations.

Data Insight: A 2023 study by the World Bank found that businesses with high outstanding balances are more likely to turn to external financing, with an average increase in borrowing costs of 2.5%.

Indirect Impacts

Erosion of Trust and Business Relationships

Timely payments are crucial in maintaining healthy business relationships. Delayed payments can not only lead to mistrust but also strain ties between a business and its clients, suppliers, or partners.

Case Study: An IT company consistently experienced late payments from a key client. Over time, this led to strained interactions, with the IT firm becoming hesitant to take on more significant projects for the same client.

The Negotiation Standstill

With rising mistrust, renegotiating terms, securing discounts, or even discussing future collaborations becomes challenging. The shadow of the unpaid balances looms large, often making such conversations fraught with tension.

Reputation and Market Perception

In our digital age, a business's reputation is paramount. Companies known for late payments or substantial outstanding balances can see their market reputation tarnished. This negative perception can deter potential partnerships and give competitors an edge.

Lost Client Confidence

For clients or customers, a business's financial health and discipline often translate to its efficiency and reliability. Clients may hesitate to renew contracts or recommend your services if they perceive financial mismanagemen

Data Insight: A 2022 survey by the US Chamber of Commerce found that 60% of businesses have lost clients due to late payments, with an average revenue loss of $10,000.

Operational and Supply Chain Disruptions

Outstanding balances can lead to a chain reaction of operational inefficiencies. Whether it's halting projects, delaying payroll, or interrupting supply chains, the cascading effects of delayed funds can be debilitating.

Case Study: GreenTech Industries, a toy manufacturer, faced stockouts during peak season because of reduced inventory purchases attributed to significant outstanding balances.

Payroll and Employee Morale

Ensuring employees are paid timely is crucial for morale and productivity. Challenges in cash flow can result in payroll delays, causing distress among staff and potentially tarnishing a company's reputation as an employer.

Example: A prominent spa in Miami faced such a predicament when outstanding balances forced them to postpone payroll, leading to employee distress.

Project Delays and Contractual Challenges

Outstanding balances can halt crucial projects as funds for execution may be unavailable. This can erode client trust and even lead to contractual penalties.

Data Insight: A 2023 report by the UK Small Business Federation found that 34% of small businesses have experienced project delays due to late payments, with an average delay of 2 weeks.

Decision-making and Growth Restrictions

Outstanding balances can also introduce uncertainty into decision-making processes. This uncertainty can delay or alter pivotal business decisions, stunting growth and giving competitors an advantage.

Case Study: A fashion startup, for example, missed a vital advertising window during the holiday season while waiting on substantial payments.

Outstanding balances can have a significant impact on all aspects of a business, from its finances and operations to its relationships and reputation. While the direct impacts are primarily financial, the indirect consequences can be even more far-reaching, affecting the very core of business operations and strategic decisions. It is therefore important for businesses to understand how outstanding balances are represented in accounting.

Accounting Representation of Outstanding Balances

Understanding outstanding balances in the realm of accounting is pivotal for businesses. It's not just about acknowledging a debt; it's about accurately representing that debt on the books. By doing so, businesses get a clearer picture of their financial health and are better equipped to make informed decisions. In accounting, an outstanding balance represents the amount that remains unpaid by a customer after purchasing goods or services on credit. It's the residue of the debt post any partial payments, interest accumulations, or penalties. Here's a dive into the intricacies of how outstanding balances make their mark in accounting.

The Journal Entry for Outstanding Balance

In accounting books, every transaction requires a journal entry. For outstanding balances, entries depend on the nature of the transaction.

When a Sale is Made on Credit:

Debit: Accounts Receivable (Value of Sale)

Credit: Sales Account (Value of Sale)

For instance, if TechGiant Ltd. sold software worth $10,000 on credit:

Debit: Accounts Receivable $10,000

Credit: Sales Account $10,000

When a Partial Payment is Received:

Debit: Cash/Bank (Amount Received)

Credit: Accounts Receivable (Amount Received)

Using the above example, if TechGiant Ltd. received $4,000 against the $10,000 outstanding:

Debit: Cash $4,000

Credit: Accounts Receivable $4,000

Calculating the Outstanding Balance: The Formula

Calculating the outstanding balance is crucial for businesses to track the amount they are owed. The formula is straightforward:

Outstanding Balance = Initial Amount - Payments Received + Accrued Interest + Any Penalties

For example, if TechGiant Ltd. had an initial outstanding amount of $10,000, received a payment of $4,000, accrued an interest of $200, and had no penalties:

Outstanding Balance = $10,000 - $4,000 + $200 = $6,200

Implications of Outstanding Balances in Financial Statements

Outstanding balances directly impact two primary financial statements:

- Balance Sheet: The outstanding balance will increase the "Accounts Receivable" under current assets, reflecting the amount due from customers.

- Income Statement: While the sale (on credit) will be recorded under revenues, any bad debts or write-offs related to outstanding balances will appear as expenses, potentially decreasing net income.

Case Study: CraftCreations, a handicraft business, noted a steady rise in its outstanding balances. Upon a thorough analysis of its books, it realized that a significant chunk of its "Accounts Receivable" was from clients who consistently delayed payments. By highlighting this in its income statement and recognizing potential bad debts, CraftCreations took proactive measures, like tightening its credit policies, to prevent further financial strain.

In essence, the representation of outstanding balances in accounting is not just an exercise in record-keeping; it’s an insightful process that can reveal much about a company's financial health. By understanding how these balances feature in the accounts and how to calculate them accurately, businesses can take the necessary steps to manage and reduce them, ensuring a healthier financial future. While understanding the accounting representation of outstanding balances is crucial, it is equally important to understand their broader implications.

The Hidden Costs and Ripple Effects of Outstanding Balances

Outstanding balances aren't just numbers on an invoice—they're powerful factors influencing a business's financial health and stability. While their immediate impact might be tangible in terms of liquidity and working capital, the ripple effects are broader, touching upon various operational and strategic facets of a business. This section delves into these often-underestimated consequences, showcasing the hidden costs and chain reactions instigated by unpaid dues.

Economic Impact

Lost Opportunity Costs: Money that remains uncollected could have been reinvested into the business, used for expansion, R&D, or marketing initiatives. Every day that an invoice remains unpaid, businesses miss out on potential growth opportunities.

Increased Financial Costs: Businesses often need to cover the cash flow gap caused by unpaid invoices. This might mean taking out short-term loans or overdrafts, which come with interest costs. Over time, this interest accumulates, increasing the financial burden on the company.

Operational Hurdles: Staff time spent on chasing unpaid invoices diverts resources from core business activities. It's not just about the finance department; sales teams might get involved in follow-ups, affecting their productivity.

Case Study: HealthyHues, a cosmetics startup, faced consistent issues with outstanding balances from a handful of retailers. Over a year, these unpaid invoices amounted to over $150,000. Due to the cash flow strain, HealthyHues had to delay a major product launch and took on a loan at a high interest rate. The combined opportunity and financial costs significantly stunted their growth in that fiscal year.

The Influence on Your Business Credit Score

Just as individuals have credit scores, businesses too have credit reports that reflect their financial reliability. Outstanding balances, especially if they are due to disputes over goods and services, can tarnish a business's creditworthiness.

- Delayed Payments: The longer an invoice goes unpaid, the more likely it will be reported to business credit bureaus. Frequent late payments can drastically reduce a company's credit score.

- Debt-to-Income Ratio: A higher outstanding balance increases a company's debt-to-income ratio, a critical factor in determining business credit scores.

- Impact on Future Borrowing: A lower credit score can make it harder for businesses to secure loans or lines of credit. Even if they do manage to obtain financing, it might be at a much higher interest rate.

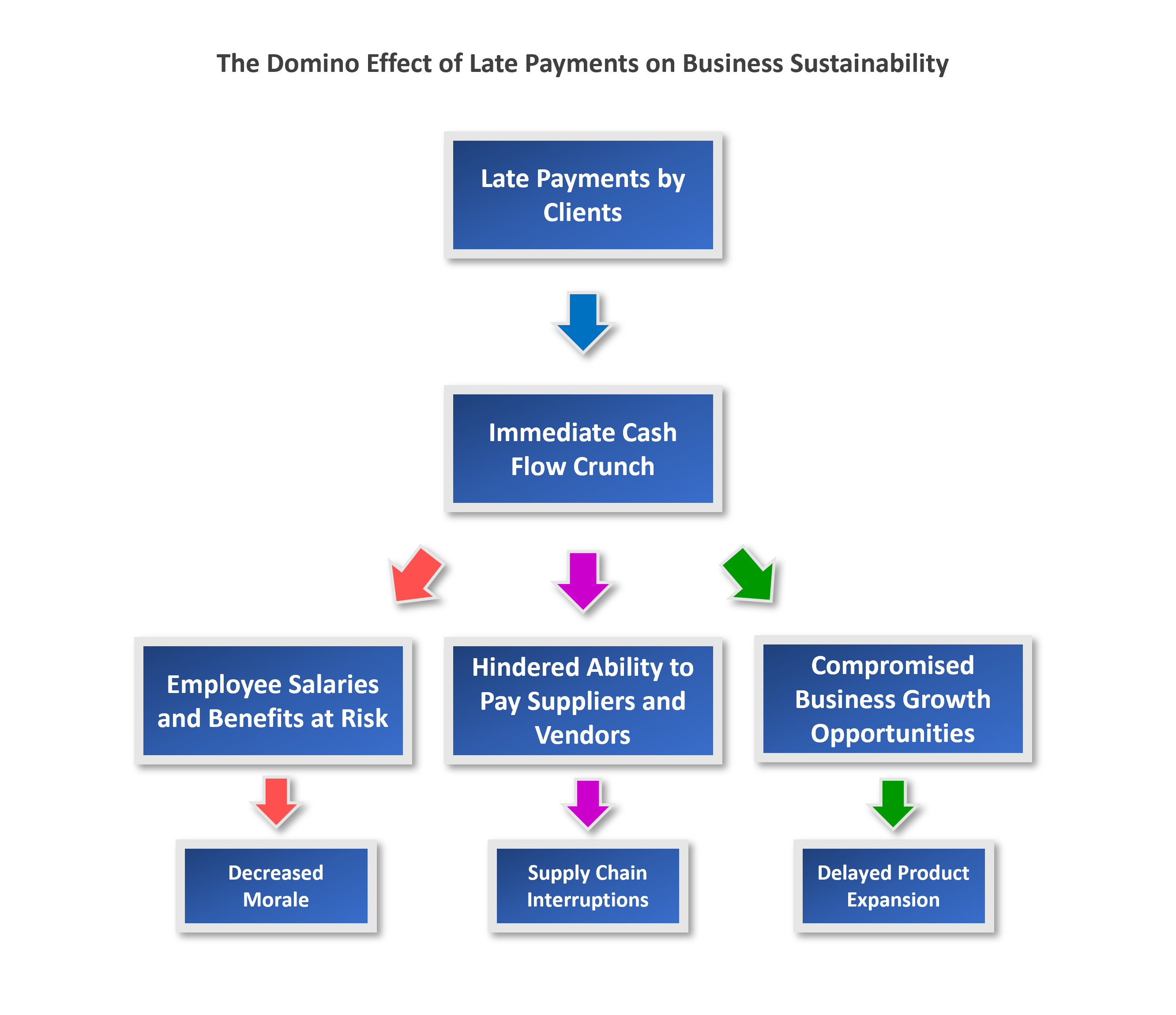

The Domino Effect of Late Payments on Business Sustainability

Every business, irrespective of its scale, thrives on a fundamental cash flow rhythm: money comes in from clients and goes out to vendors, employees, and other operational costs. Yet, when this rhythm is disrupted due to a cycle of late payments, it triggers a chain reaction that can send ripples across the entire business ecosystem. Here's an in-depth exploration into the intricacies of this domino effect and how it can choke a business's lifeline.

Immediate Cash Flow Crunch: Late payments mean funds expected to be in your account aren't there. This leads to an immediate strain on the working capital, making it challenging to cover regular operational costs. The inability to cover day-to-day expenses can bring a business's operations to a standstill.

Case Study: TechCrafters, a small software development firm, had three major clients delay their payments by two months. Consequently, they faced a cash deficit and struggled to pay for their cloud hosting services, thereby risking website downtimes.

Hindered Ability to Pay Suppliers and Vendors: As the cash flow starts straining, businesses find it difficult to settle their own bills. This not only leads to strained relationships with suppliers and vendors but might also lead to supply chain disruptions.

Employee Salaries and Benefits at Risk: One of the most detrimental impacts of the late payment cycle is the potential delay in disbursing employee salaries. This can demoralize the workforce, leading to reduced productivity, and in severe cases, employee attrition.

Case Study: GreenFarm Fresh, a mid-sized organic produce supplier, faced consistent late payments from their distributors. When this led to a delay in salary disbursement for two consecutive months, they lost three of their senior team members to competitors.

Compromised Business Growth Opportunities: The funds tied up in outstanding balances could have been invested in growth opportunities. Whether it's launching a new product, expanding to new geographies, or upping the marketing game, a cash crunch can halt these initiatives.

The Long-Term Credit Implications: Repeatedly dipping into overdrafts or taking out emergency loans to bridge the cash flow gap affects the business's credit score. Over time, this can make borrowing more expensive or even inaccessible.

The Amplified Domino Effect: The ripple effect doesn't stop at one business. When one business can't pay its suppliers due to its own outstanding balances, those suppliers may, in turn, face their own cash flow challenges, creating a cascading impact through the business ecosystem.

Case Study: Consider a local bakery that supplies to a popular cafe. If the cafe delays payments to the bakery because its own clients aren't paying up, the bakery might struggle to pay the flour supplier. This cycle continues, creating a web of financial strain across multiple businesses.

Breaking the Cycle

Late payments can have a serious impact on businesses. They can tie up cash flow and disrupt operations, making it difficult to achieve long-term goals. The first step to combating late payments is to recognize the risks they pose. Businesses can then take proactive steps to manage these risks, such as implementing rigorous invoicing practices, using technology to track payments, and communicating openly with customers.

However, even with preventive measures in place, late payments can still occur. This is where trade credit insurance can help. Trade credit insurance is a safety net that protects businesses against the financial losses caused by customer insolvency or overdue payments. It can also provide businesses with valuable credit risk information and market intelligence.

Allianz Trade's credit insurance offers businesses peace of mind. It guarantees the safety of their accounts receivable and helps them expand sales securely, both locally and internationally. In a climate where late payments can be a major obstacle to growth, trade credit insurance is an invaluable tool. As businesses explore new customers and seek to increase their credit lines with existing ones, trade credit insurance can help them navigate the turbulent waters of cash flow challenges and achieve their long-term goals.

Explore Allianz Trade's Trade Credit Insurance Solutions Now