Executive Summary

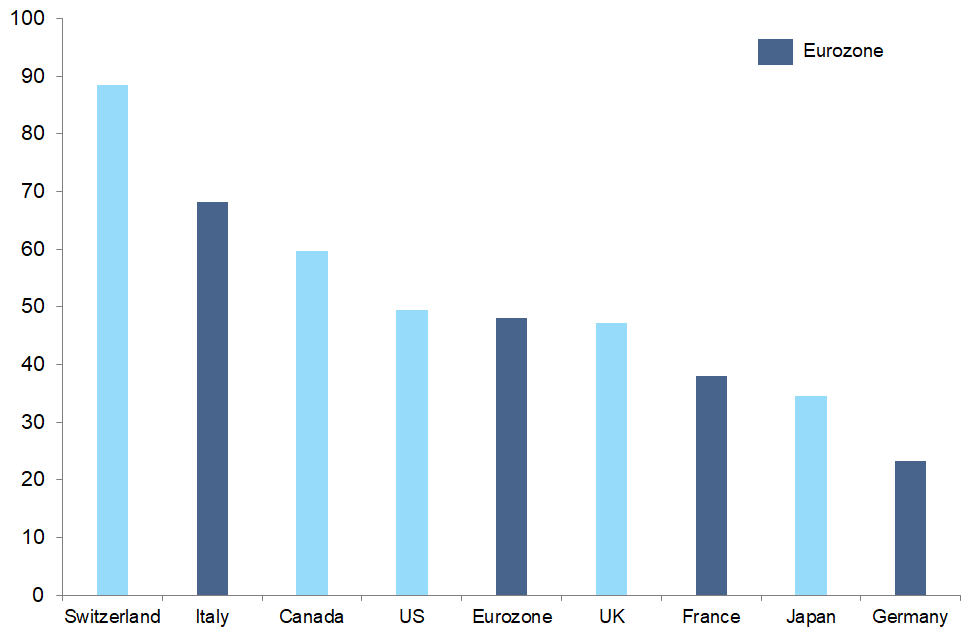

- In response to the Covid-19 crisis, the debt-to-GDP ratio in advanced economies will rise to an all-time high of 130% of GDP this year. At the same time, long-term interest rates are at an all-time low.

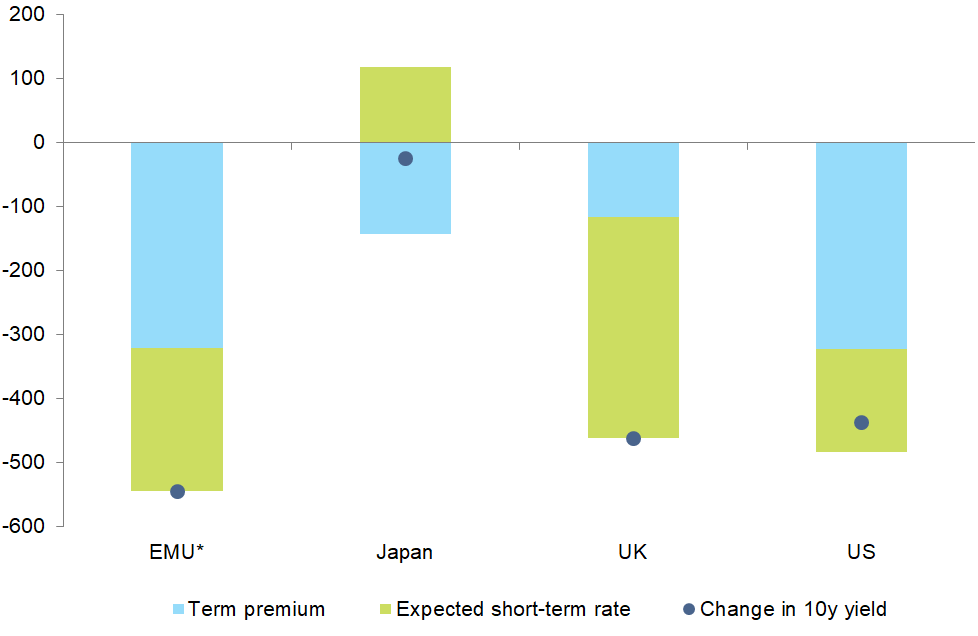

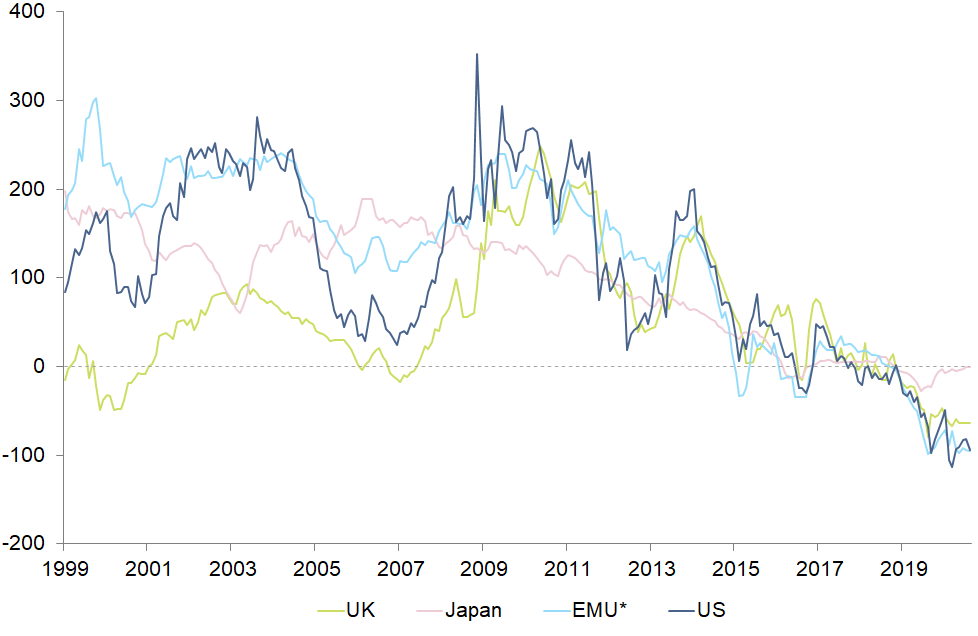

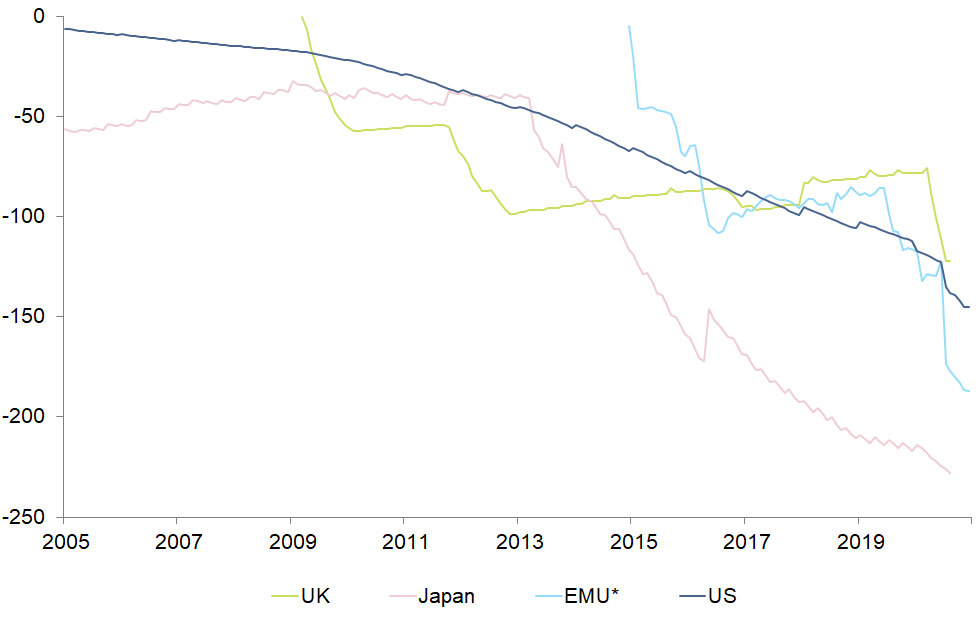

- The decline in long-term interest rates is due in large part to the fall in the term premium. This has now turned negative globally. For the 10y maturity, we estimate the global term premium currently at -60bps.

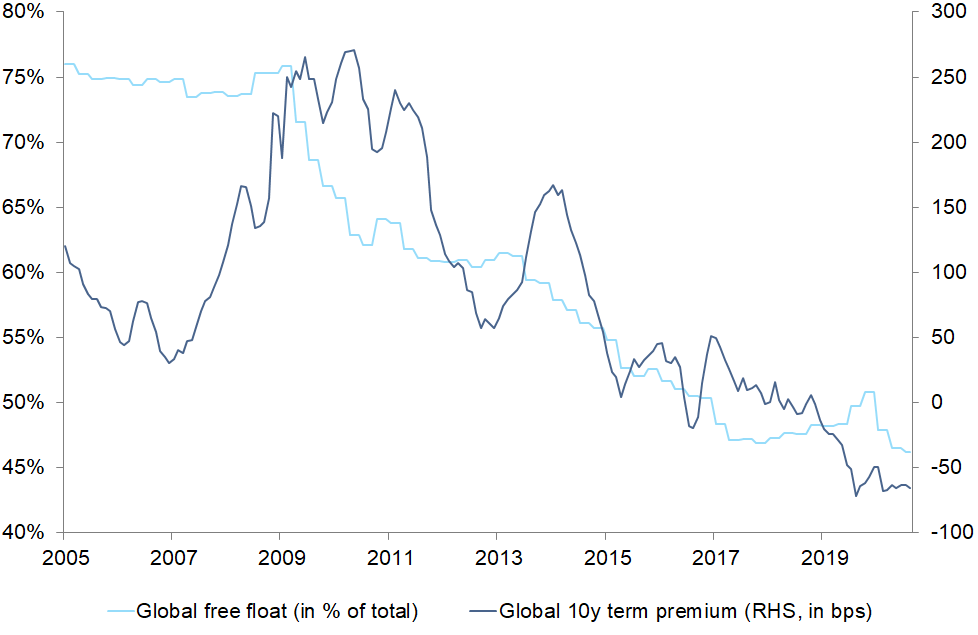

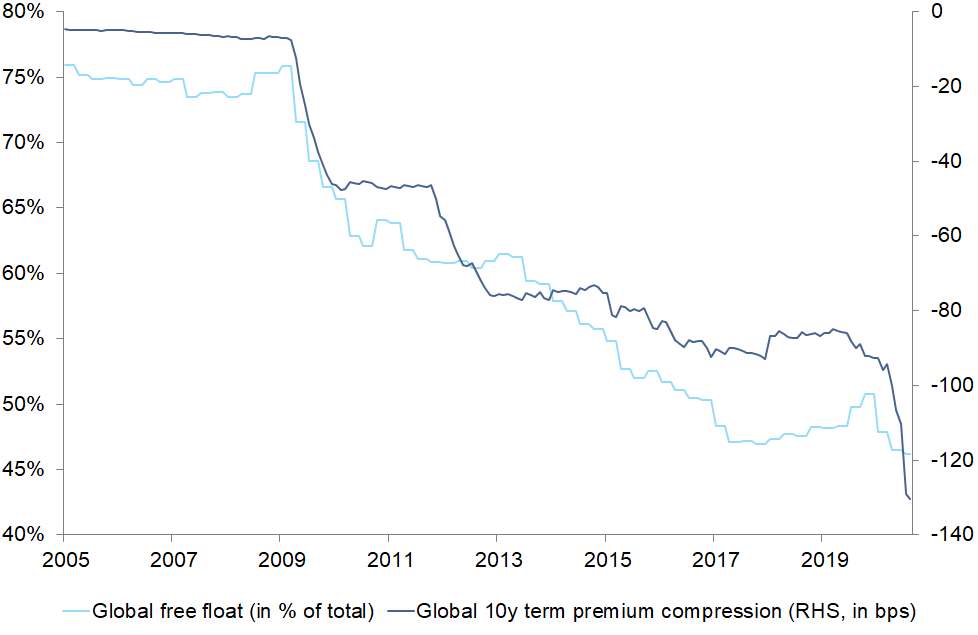

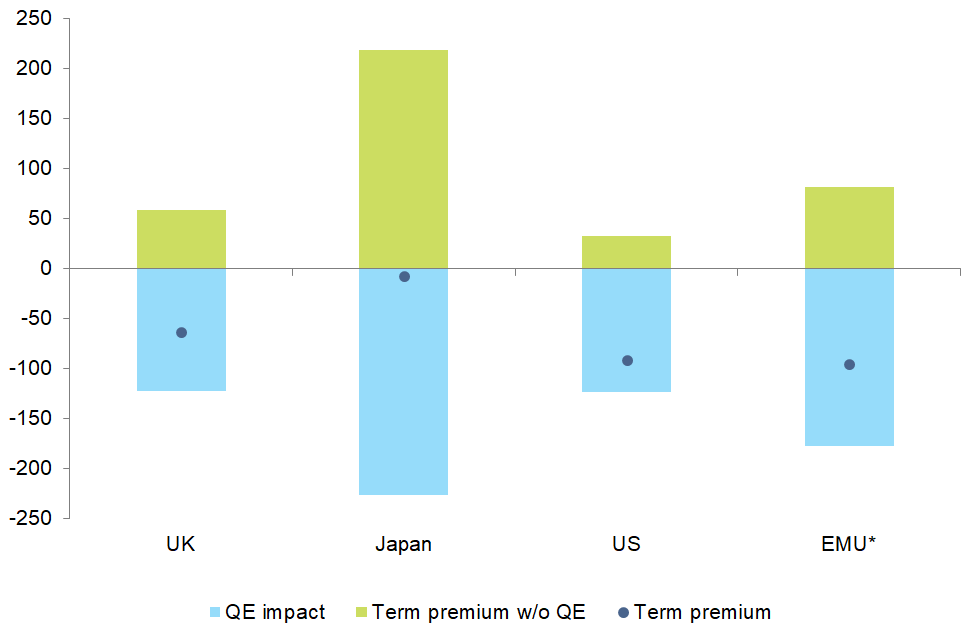

- The inversion of the term premium from a receivable risk premium to a payable safety premium is due to the amplification of unconventional monetary policy (especially Quantitative Easing). We currently estimate the global term premium compression by central banks at -130bps. Depending on the aggressiveness of the current QE programs, it could reach up to -200bps by the end of 2021.

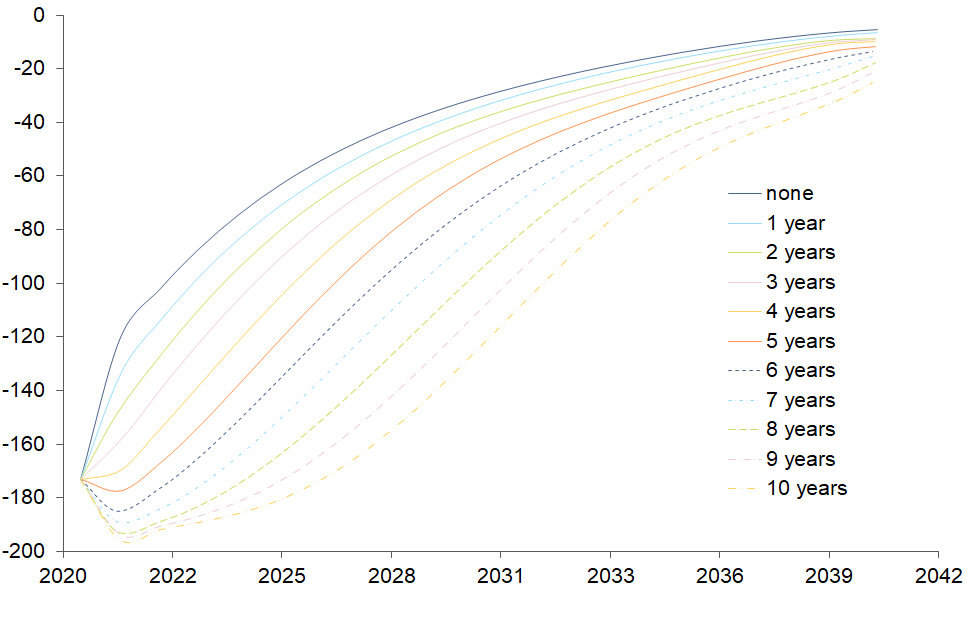

- The yield-dampening effects of the term premium compression are long-term, since QE is followed by a phase of reinvestment.

- This environment presents several challenges for investors, including an increasingly hybrid risk profile of safe government bonds, which reduces their diversification characteristics to risky assets, and the increasing loss of return potential through carry.

- Possible responses are to compensate for the carry return with more duration (i.e. ultra-long bonds) or credit risk, or a more active management style to benefit from short-term dislocations on preferred curve segments.

A puzzle of premia - decomposition of nominal interest rates

The public response to the Covid-19 crisis has resulted in a massive and globally synchronized increase in sovereign debt, especially in advanced economies. This year, the debt-to-GDP ratio will reach an all-time high of 130%, even exceeding the level reached during World War II. This all-time high in public debt coincides with an all-time low for long-term government bond yields. The trend of falling interest rates has been going on for about 40 years, related to structural changes in demography and productivity (secular stagnation). However, since the 2008 Global Financial Crisis, unconventional monetary policy, especially large-scale bond purchases (Quantitative Easing), has also contributed to this downward trend. In this paper, we estimate the influence of central banks on government bond interest rates in advanced economies to show how sustainable this influence is, and how it should change the strategy of fixed income investors.

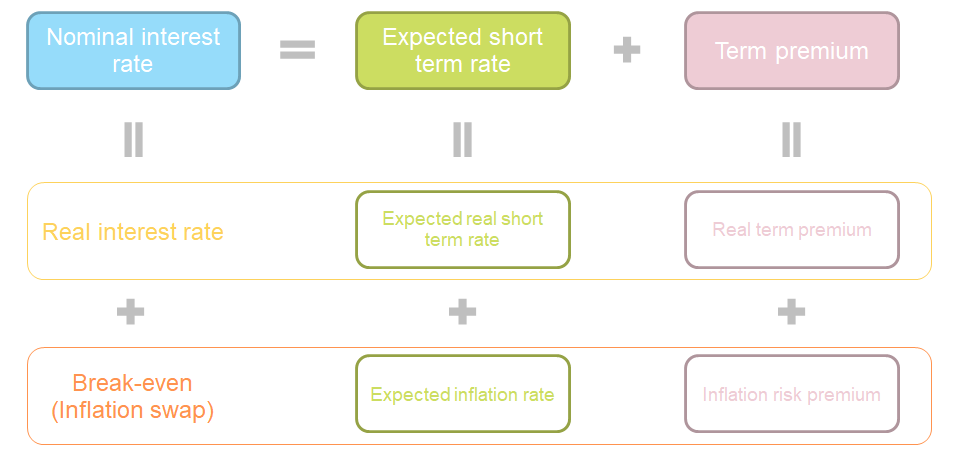

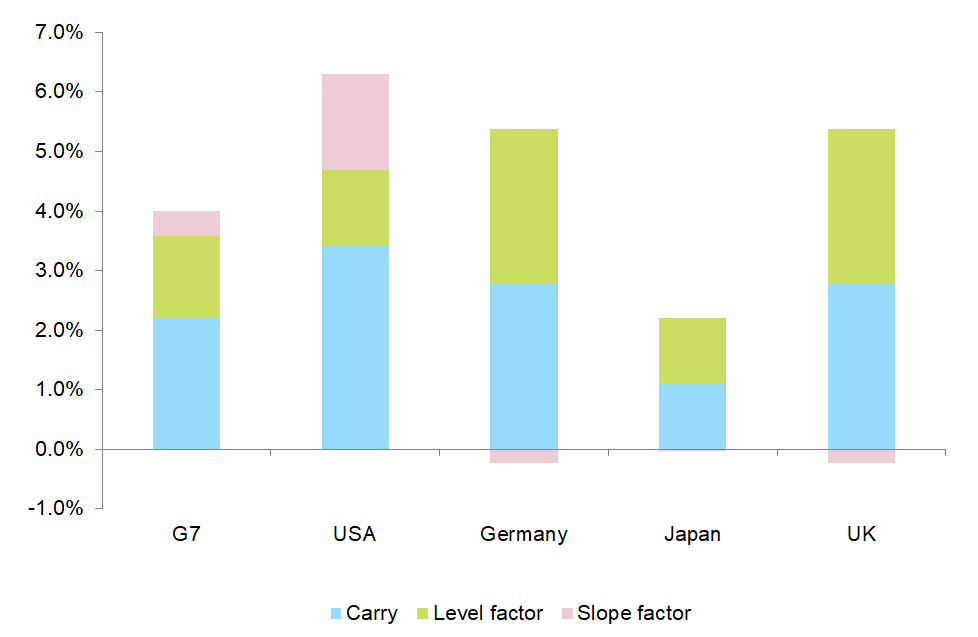

First, we have to break down nominal interest rates. We use a term structure model with two principal components: a level factor (expected short-term rate) and a slope factor (term premium) (see Figure 1). The term premium represents the investor’s risk reward for holding long-term bonds instead of a rolling investment in short-term interest rates. It is not to be confused with the simple steepness. The term premium is a risk premium that arises from the deviation of the actual term structure from a stylized term structure that reflects the so-called expectation hypothesis, which claims that yields on default-free government bonds should equal current and future short-term rates.

Figure 1: Term structure model – decomposition of nominal yields