Executive Summary

- Strong cash balances (EUR690bn above pre-crisis levels in the Eurozone and more than USD765bn in the US), as well as rising profitability and capex, are cushioning most US and Eurozone companies from high input prices – for now. But as the earnings season unfolds, the most pressing question is which firms will be able to offset higher wage bills with productivity enhancement, and bear increasing borrowing costs.

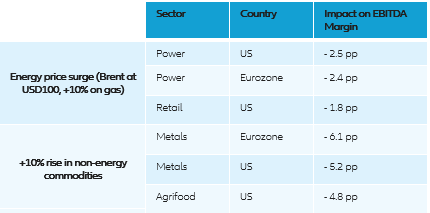

- With inflation set to remain above 2% until late 2023, corporates have the leeway to withstand a moderate monetary policy tightening cycle (around +100bp). However, should commodity prices, wages or interest rates rise more than expected, we find that the construction, power, metals and the US transport sectors are most at risk of a liquidity and profitability squeeze.

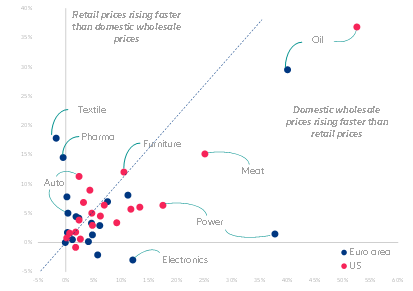

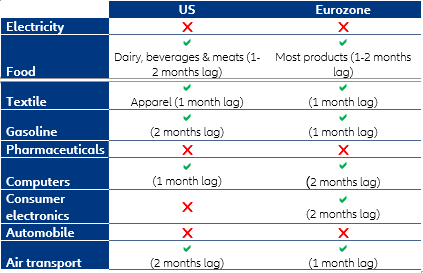

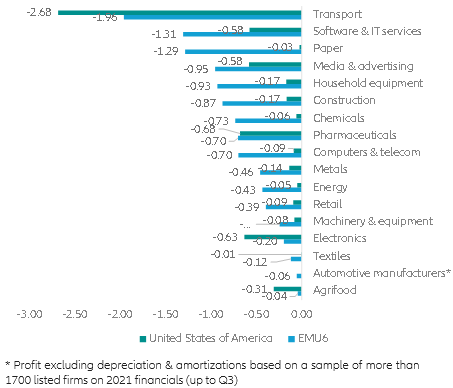

Strong cash balances, as well as rising profitability and capex, are cushioning most US and Eurozone companies from high input prices – for now. In 2021, input prices outpaced retail prices in most sectors, the result of supply-chain disruptions, the strong rebound in demand, constraints on the commodity supply and the rise of safety restocking. However, only about 40% of sectors on both sides of the Atlantic had retail prices rising faster than wholesale prices (see Figure 1). Over the long-term, 53% of Eurozone sectors (including automotive, sporting goods, pharmaceuticals) have seen retail prices grow faster than their wholesale prices against 25% for the US. And while a year-end survey showed that a majority of firms are planning to raise prices, we find that only a handful really have the ability to pass on higher input prices (see Table 1) – notably oil, air transport and textiles, as well as some sub-sectors of food manufacturing. In addition, some industries could face the prospect of risking increasing prices even as demand is waning.

Figure 1 – CPI vs PPI in 2021, US vs Eurozone