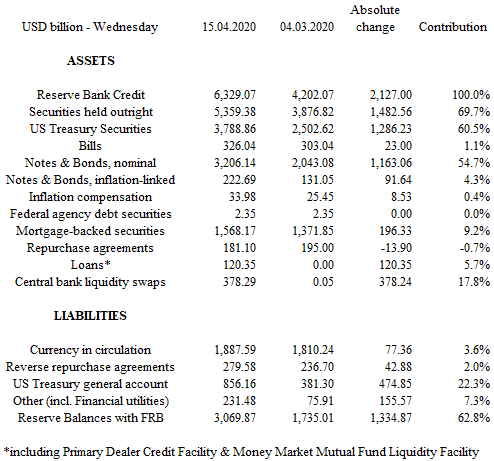

Put differently, it is crucial to look at changes in both the assets and the liabilities of the Federal Reserve: the assets for the applications of central bank’s liquidity, the liabilities to see where this liquidity has landed. As shown in Table 1, a little bit more than 60% of the USD2.1tn increase in assets comes from the buying of U.S. Treasuries. The second largest contribution (almost 18%) comes from central bank liquidity swaps. Next come mortgage-backed securities (almost 10%) and loans (5.7%), an item which comprises the Primary Dealer Credit Facility and the Money Market Mutual Fund Liquidity Facility. As of 15 April, repurchase agreements (loans collateralized by securities) were virtually unchanged from 04 March, but a USD250bn increase up to 18 March, driven by market volatility induced margin calls, unwound past the settlement dates of derivatives transactions.

Admittedly, it is only on 23 March that the Fed announced its plan to purchase corporate bonds in both the primary and secondary markets. And, of course, by merely announcing plans to broaden its interventions in credit markets, the Fed may have made them superfluous, at least until fresh “bad” news like defaults hit the credit markets again. Nevertheless, it seems fair to say that for the time being the private non-financial sector has to a very limited extent directly benefited from the Fed’s interventions. For example, the Commercial Paper Funding Facility announced on 17 March is still to be activated.

A review of the Fed’s liabilities supports this assessment. The reserves deposited by banks with the Fed have absorbed 63% of the USD1.8tn increase in the Fed credit. With 34% of that tally, the U.S. Treasury general account has been the second largest absorber. Next comes the reserves held by clearing houses (7%), currency in circulation (4%) and reverse repurchase agreements (2%). Evidence that fiscal policy does come to the rescue of the real economy will be seen when the U.S. Treasury general account shrinks: for the time being, the U.S. Treasury is merely accumulating a war chest.

To complete this investigation of the transmission of monetary policy, let’s look at the weekly assets of commercial banks in the U.S. As of 08 April, the latest data point, almost two thirds of the USD1.5tn increase in banks’ assets since 04 March was attributable to cash assets, the bulk of which is made of reserves at the Fed. Interestingly, federal funds, i.e. the reserves lent and borrowed in the interbank market, have shrunk by USD235bn, so that on a net basis, more broadly defined cash assets explain almost half of the increase in banks’ assets. In contrast, commercial and industrial loans contribute only a third of the increase in banks’ assets. Anecdotal evidence suggests that a large part of this increase in commercial and industrial loans has been triggered by companies rushing to tap back-up credit lines (revolving credit facilities) negotiated before the crisis started. In other words, this expansion in commercial and industrial loans reflects less the banks’ willingness to lend than their corporate clients’ dash for cash. The contraction in consumer loans points in the same direction. The start of the Q1 earnings season is showing that banks are expecting significant increases in loan losses. Without some form of loan guarantee provided by the U.S. Treasury, fresh bank lending is likely to be problematic, if not quarantined.