Sharpest quarterly contraction on record

The Covid-19 crisis has hit the Eurozone economy like a meteorite. According to a preliminary flash estimate provided by Eurostat, Eurozone GDP declined by -3.6% q/q in Q1 2020 – the sharpest decline on record. To compare and contrast, in Q1 2009, at the height of the Great Financial Crisis, Eurozone GDP contracted by -3.1% q/q. Available national GDP releases confirm that the hit to economic activity was widespread across the region, with no economy immune to the shock: Italy (-4.7% q/q), France (-5.8% q/q) and Spain (-5.2% q/q) recorded the sharpest contractions, but GDP declines in Belgium (-3.9% q/q) and Austria (-2.5% q/q) still proved dramatic.

Black hole economics

Today’s GDP releases clearly have to be taken with a pinch of salt. With little hard economic data available for the month of March, statistics offices in fact underlined the even higher-than-usual uncertainty surrounding their Q1 growth estimates. Given the lack of administrative data, the Belgium Statistics office, for instance, stated that it used an adapted methodology for which a wide range of available information, including news releases, websites and contacts with companies and various surveys, were considered as inputs to form assumptions about the economic impact of Covid-19. Expect significant revisions to come in the months ahead.

Q1 is only the tip of the iceberg, Q2 will be MUCH worse

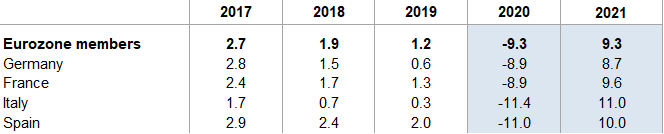

If the Q1 data makes you nervous, don’t ask about what is in store for Q2 2020. We expect to see a double-digit quarterly GDP contraction to the tune of close to -17% q/q in the three months between April and June. After all, confinement measures were imposed in most Eurozone economies only in mid-March and started to fully bite in April, which is when we expect economic activity levels to have dropped 30%-40% below normal. While we are seeing light at the end of the tunnel – with economies showing signs of a timid recovery in line with the gradual easing of containment measures in several countries from early May onwards – a quick return to pre-Covid-19 daily life is very unlikely. After all, we expect consumption and investment activity to remain lackluster in the post-crisis regime until a vaccine is in place as: (1) some containment measures will remain in place (most notably restrictions on large gatherings and travel, suggesting that these sectors may not fully restart in 2020) (2) consumers will remain cautious particularly in the early stages of deconfinement (i.e. we will not all go to the cinema in May) (3) it will take some time for laid-off workers or those on reduced hours to be reabsorbed in the labor market, which should keep a lid on consumer spending (4) external demand could remain impaired in the near-term with countries not all deconfining at the same time so that investment activity will also prove subdued at best. Therefore it should take until mid-2021 for Eurozone GDP to recover to its pre-Covid-19 levels. However, in some countries, particularly those that boast a large value-added share in services and tourism, the recovery process could well last until mid-2021 as these sectors may see longer-lasting damage from the crisis. Assuming no further substantial fiscal stimulus down the line in an effort to jump-start the economic recovery, the Eurozone economy looks set to contract by -9.3% in 2020.The rebound in 2021 of +9.3% is based on the assumption that the discovery and wide-spread distribution of a vaccine allows for a return to normalcy.

In France, GDP contracted sharply by -5.8% q/q, quite in line with our estimate of -6.1%, but much above consensus expectations of -4%. This is the sharpest decline in the history of the quarterly series, i.e. since 1949. This contraction was much stronger than those recorded in Q1 2009 (–1.6% q/q) or Q2 1968 (–5.3%), episodes of recent recessions. The fall in household consumption expenditure (–6.1%) was slightly more moderate than our expectations, whereas the dramatic drop of investment (–11.8%) was much stronger than expected. Exports fell quite drastically (–6.5%), while the fall in imports was slightly less marked (-5.9%). As expected, companies built inventories, driven by the unprecedented domestic and external shock (+0.9pp) as all non-essential activity ceased under the lockdown. Meanwhile, government spending was down -2.4% q/q in Q1 as the closure of public administration offices weighed on expenditure. Going forward, we expect GDP to contract massively by -16% in Q2 q/q as activity will remain around 30% below normal levels over the lockdown period, which is expected to last at least until 11 May. Over the year, we expect real GDP to contract by -8.9% as we only foresee a very gradual resumption of activity during deconfinement, which we expect to last for three to four months. We project manufacturing and construction activity to resume faster and reach pre-crisis levels at year-end, while services would remain below until Q2 2021, in the absence of a treatment or vaccine. Regarding domestic demand, both consumer spending (-13.1%) and investment (-13.1%) will contract sharply in an environment of prevailing uncertainty. Net exports are expected to be positive (+1%) in 2020, on account of imports (-13.3%) dropping more than exports (-10.6%). The change in inventories is expected to be slightly negative (-0.8%), reflecting the de-stocking of companies seeking to improve their cash positions at the exit of the crisis, keeping deflationary pressures high. The risks to our baseline scenario (U-shaped recovery and a rebound in GDP growth of +9.6% in 2021) remain on the downside.

In Italy, the -4.7% q/q decline in real GDP in Q1 was clearly less than consensus had expected (-5.4% q/q). This means that despite the scale of the sanitary crisis, the stringency of the lockdown and the regional concentration of the pandemic in the economic stronghold of north Italy, it suffered a much smaller decline in real GDP than France. However, we think that there is a lot of scope for significant downward revisions in the coming months. The unemployment figures for March released earlier today (decline from 9.7% to 8.4%) already showed that there are admittedly problems in correctly recording the data in the lockdown.

Even though the government implemented a gradual deconfinement plan (starting on 4 May), economic activity is likely to deteriorate much further in Q2, when the decline in investment and the loss of tourism revenues will have a much stronger negative impact (at least -16% q/q). Only in H2 should we see a gradual return to economic normalcy. Nevertheless, real output is likely to fall by -11.4% this year, the worst recession since WWII. Even with a strong rebound in 2021 (est. +11%), Italy's real GDP is still likely to be 3% below the level before the Covid-19 crisis.

According to preliminary data, in Spain GDP contracted -5.2% q/q in Q1 after growing +0.4% q/q in Q4 2019. In y/y terms, GDP contracted -4.1% after growing +1.8% in Q4 2019. The national statistics institute used the number of hours worked, which dropped -5% q/q, to refine its estimate of March activity. The drop in GDP was mostly due to internal demand, which subtracted -5.3pp from growth, while the fall in exports was almost perfectly matched by the fall in imports. From a sector perspective, construction activity was the most hit, dropping -8.1% q/q, followed by services -5.6%, with a massive trop in trade, transport and hospitality (-10.9%) and arts and recreational activities (-11.2%), as expected. In Q2, we expect a -19% q/q drop as the shock could be three times stronger due to the lockdown lasting 1.5 months, followed by subdued activity during deconfinement (80% of pre-crisis activity). Overall, in 2020, we forecast an annual contraction of -11% in Spanish GDP, on the back of a deep contraction in private consumption (-15.7%) and investment (-12.7%). We see insolvencies rising +24% this year as a result. The return to 2019 nominal GDP could only happen by the end of 2021.

Figure 1: Eurozone GDP growth