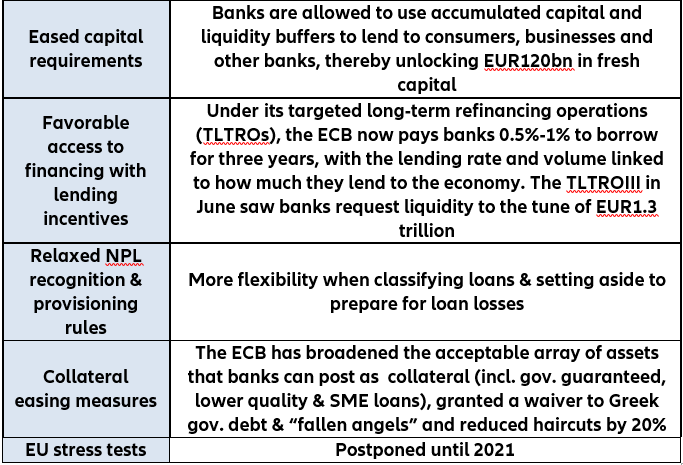

A Faustian bargain to limit short-term economic pain: Since the onset of Covid-19, policymakers have taken swift and unprecedented action (including EUR2.1tn in state-guaranteed loans in the big four Eurozone countries alone and EUR1.3tn in cheap ECB loans) to sweeten the deal for banks to ensure that they provide an emergency liquidity lifeline to the private sector, notwithstanding rising credit risk. Banks have been assigned a key role in mitigating the economic shock from Covid-19 and supporting the recovery. In fact, this is in sharp contrast with Europe’s financial and debt crises a decade ago, which originated in the sector and saw banks reluctant to extend credit to protect their balance sheets, which in turn exacerbated the downturn. So far, banks have weathered the initial strain from the Covid-19 crisis quite well which, in turn, facilitated the access to credit for non-financial corporations. Next to enhanced resilience in the form of stronger capital and liquidity positions this is in large part the result of a somewhat Faustian bargain: Policymakers have taken swift action to sweeten the deal for banks to ensure that they continue to provide an emergency liquidity lifeline to the private sector, despite rising credit risk. The measures range from central banks showering banks with new funding options and supervisors easing capital as well as supervisory liquidity requirements to national governments extending generous public guarantees to reduce direct exposure. Some measures, such as the favorable rates on the June TLTRO, provide an outright and ongoing subsidy (around EUR16bn over the next 12 months, which will more than make up for the tax levied on deposits) for banks that at least maintain their lending activities to the real economy.

Figure 1: Covid-19 banking sector support measures

Figure 1: Covid-19 banking sector support measures