What are Euler Hermes’ responsibilities?

- It is our responsibility to continually monitor your buyers’ financial health, including alerting you in the event that a change in their status impacts our ability to cover the buyer. An important part of our process for conducting this ongoing analysis is proactive outreach to your buyers to request updated financials – a step which we can often work in partnership with you to be more successful.

- Indemnification of covered buyers – In the event of a bad debt loss on one of your covered buyers, you may submit a claim and we will pay it promptly, per the parameters of your policy wording.

- Provide you with timely and actionable economic intelligence, strategic forecasting, and market-specific analysis that can help guide your strategic business decisions.

What are your primary responsibilities?

- Submitting credit limit requests and monitor status in EOLIS.

- Submitting overdue declaration on all covered past due buyers in EOLIS.

- Completing a turnover declaration to declare insured turnover at the end of the policy year in EOLIS.

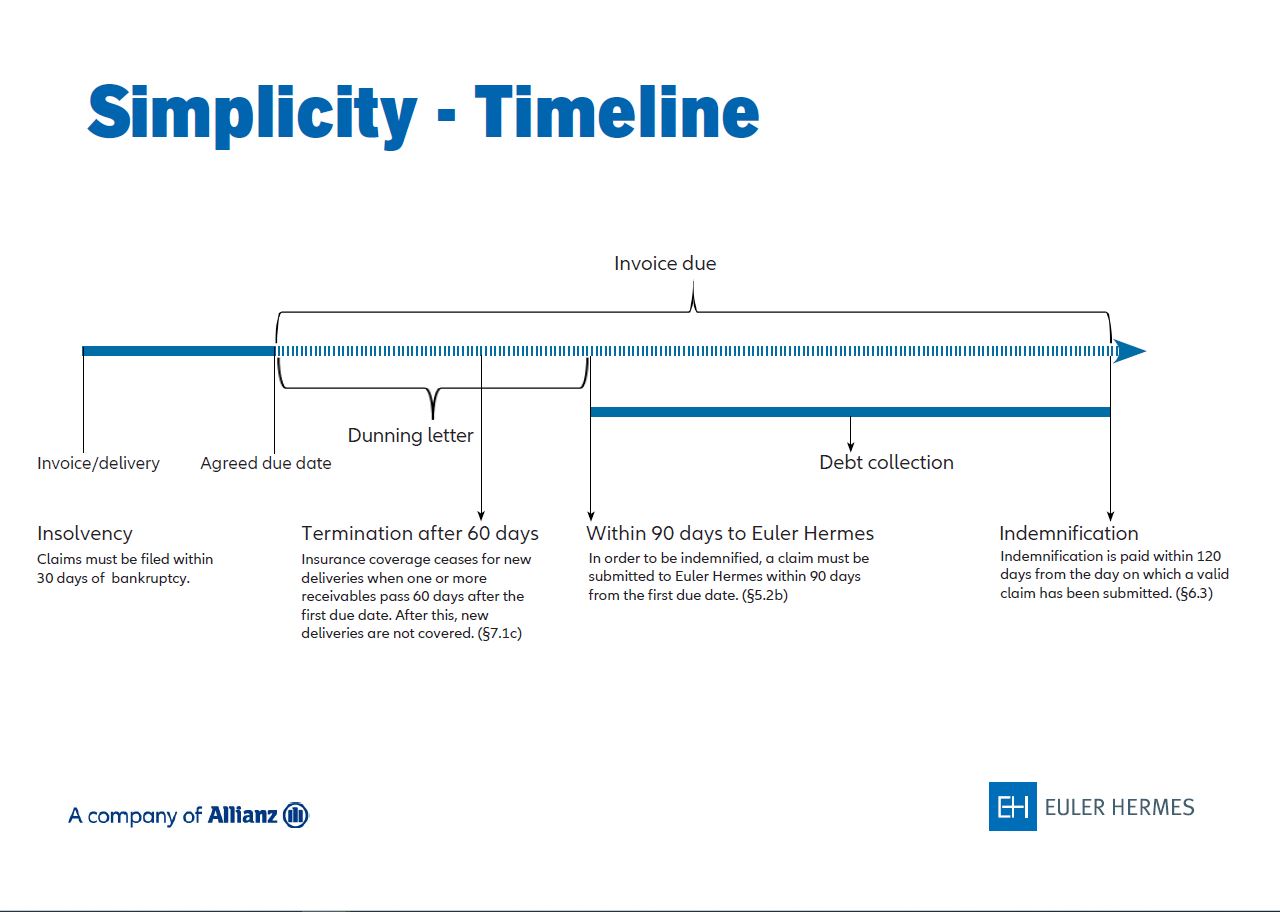

- In the event of a claim, customers must submit a claim form and all accompanying documents by their claim filing deadline.

- Ensure you follow the debt collection policy in case of overdues.

- Collaborate with us to obtain financials – One important source of information from which we base our credit limit decisions is the exclusive information Euler Hermes receive when we contact buyers in order to obtain updated financial statements. Our customers’ partnership in this effort can help improve our mutual success. Consider providing your permission for us to disclose your company’s name to your buyers when we contact them for financials, as this makes them statistically more likely to respond.